For many homeowners, the tax benefits are still offering relief in this tough economic time..

Tax Time Less Taxing for Home Owners

Washington, March 15, 2011

“Owning a home offers myriad benefits throughout the year, but some of the financial advantages of home ownership are most apparent at tax time,” said NAR President Ron Phipps, broker-president of Phipps Realty in Warwick, R.I. “As many of today’s hard-working American families are feeling a financial squeeze, the tax benefits that can come from owning a home can be a welcome relief.”

A number of tax deductions and credits are still available for home owners; these include deductions – with specific limits – for mortgage interest and capital gains on home sales, and credits for certain energy-efficient home improvements. Even with these benefits, home owners pay 80-90 percent of all U.S. federal income taxes.

“It’s been suggested that many of today’s tax incentives for home ownership primarily benefit wealthy individuals, but that’s simply not true,” said Phipps. “As today’s public debate continues about what home ownership means for families, communities, and the nation’s economy, there’s no question that for many, owning a home is still the best way to begin building wealth.”

Ninety-one percent of home owners who claim the mortgage interest deduction earn less than $200,000 a year, and the ability to deduct the interest paid on a mortgage can mean significant savings at tax time. For example, a family who bought a home in 2010 with a $200,000, 30-year, fixed-rate mortgage, assuming an interest rate of 4.5 percent, could save nearly $3,500 in federal taxes when they file this year.

“Realtors® see the very real positive impact of home ownership every day with our clients,” said Phipps. “Recent proposals to reduce or eliminate the mortgage interest deduction and remove government support of the housing finance market could have disastrous consequences for the economy, not to mention making it harder or nearly impossible for millions of families to own their own homes. We believe America must continue to invest in home ownership, for the future of our families and our nation.”

For home owner tax season tips, visit www.HouseLogic.com. HouseLogic is a free source of information from NAR that helps home owners maintain and enhance the value of their homes and engage in issues that affect their local communities.

The National Association of Realtors®, “The Voice for Real Estate,” is America’s largest trade association, representing 1.1 million members involved in all aspects of the residential and commercial real estate industries.

# # #

Showing posts with label tax credit. Show all posts

Showing posts with label tax credit. Show all posts

Monday, March 28, 2011

Thursday, December 23, 2010

"Pending Sales Are Up"

Finally! On the uptrend, pending sales increased in October since bottoming in June, according to the National Association of REALTORS.

A "pending" or "under contract" sale, is a real estate sale that is non-contingent (ex: home inspection contingency removed)and is moving forward to closing.

Read more about this at

http://www.realtor.org/press_room/news_releases/2010/12/strong_phs

Happy Holidays Everyone! Have a happy, healthy and prosperous new year!

A "pending" or "under contract" sale, is a real estate sale that is non-contingent (ex: home inspection contingency removed)and is moving forward to closing.

Read more about this at

http://www.realtor.org/press_room/news_releases/2010/12/strong_phs

Happy Holidays Everyone! Have a happy, healthy and prosperous new year!

Sunday, November 21, 2010

Tax Credit Effects on the Real Estate Market

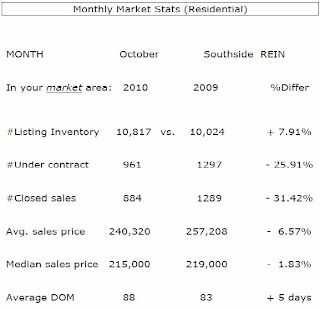

Last year's tax credit encouraged many buyers that were "sitting on the fence" to go ahead and purchase a new home. Here are the market stats for the month of October as it compares to this time last year.

REIN reports

Effects of ’09 Tax Credit Starting to Show

(Virginia Beach, Virginia – November 8, 2010)

The effects from the residential sales surge experienced in the third and fourth quarters of 2009 are now starting to be more prominent in 2010 sales totals comparisons. Traditionally, the third and fourth quarters are slower when compared to the second quarter of the year. But, in 2009 the third quarter had the highest sales total and the fourth quarter was almost equal to the second. This shift in buyers’ habits was due in large part to the federal tax credit. It caused many people who were potential buyers in the first and second quarters of 2010 to buy in the third and fourth quarters of 2009 prior to the original tax credit expiration of November 30. This date set a line in the sand for home buyers and the following extension allowed even more buyers to move their own purchase timelines to earlier dates thus “pulling forward” home sales activity. Many people across the country bought homes sooner than planned specifically for the tax credit and skewed many settled sales totals prior to the credit’s expiration.

The number of active homes for sale in the region last month remained high and increased by 8.95% when compared to October 2009. The recent levels of homes for sale have been the highest recorded for each month since February 2010. The region has maintained a level above 15,000 available listings for seven straight months, also the most on record. However, the median listing price of homes on the market in October 2010 declined by 9% when compared to October 2009. This drop is in line with the settling of home prices in Hampton Roads and is a potential sign of housing stability.

The number of under contract residential sales fell year-over-year by 28% in October. This statistic, often referred to as a leading market indicator, does not provide a very positive outlook for the near future. Most of the recent downturn in under contract may be attributed to the expiration of the federal tax credit, but other factors are also influencing the rapid drop in transactions including availability of credit and consumer expectations.

Residential settled sales plunged 32.4% in October when compared to the same time last year. The plummet was the largest year-over-year drop since January 2009, -35%. Each of the seven major cities in the area experienced sales declines ranging from a low of -21% in Norfolk to the high of -46% in Newport News. The median sales price for October 2010 was down 1.2% when compared to October 2009. The median price for homes sold seems to have bottomed for the region with its continued small differences as recorded each month. Some areas, including Virginia Beach, Chesapeake, and James City County, are starting to experience price appreciation with each area up 1% year-over-year.

The months’ supply of inventory held at ten months, but the absorption rate, the average number of homes sold over the past twelve months, continued to decline and is now at 1,480 homes per month.

The percentage of distressed listings, those that are bank owned or short sales, expanded to account for 22% of the active homes for sale and they comprised 31.7% of the settled sales total. October was, by far, the most prevalent month for distressed sales activity in our region since the housing bubble burst. Current market conditions and the overall economy do not show signs of a dramatic decrease in distressed listings. If these trends, both percent of active and sold listings, continue upward home prices within the region may decline as a result of the downward pressure these distressed homes have on local markets.

REIN reports

Effects of ’09 Tax Credit Starting to Show

(Virginia Beach, Virginia – November 8, 2010)

The effects from the residential sales surge experienced in the third and fourth quarters of 2009 are now starting to be more prominent in 2010 sales totals comparisons. Traditionally, the third and fourth quarters are slower when compared to the second quarter of the year. But, in 2009 the third quarter had the highest sales total and the fourth quarter was almost equal to the second. This shift in buyers’ habits was due in large part to the federal tax credit. It caused many people who were potential buyers in the first and second quarters of 2010 to buy in the third and fourth quarters of 2009 prior to the original tax credit expiration of November 30. This date set a line in the sand for home buyers and the following extension allowed even more buyers to move their own purchase timelines to earlier dates thus “pulling forward” home sales activity. Many people across the country bought homes sooner than planned specifically for the tax credit and skewed many settled sales totals prior to the credit’s expiration.

The number of active homes for sale in the region last month remained high and increased by 8.95% when compared to October 2009. The recent levels of homes for sale have been the highest recorded for each month since February 2010. The region has maintained a level above 15,000 available listings for seven straight months, also the most on record. However, the median listing price of homes on the market in October 2010 declined by 9% when compared to October 2009. This drop is in line with the settling of home prices in Hampton Roads and is a potential sign of housing stability.

The number of under contract residential sales fell year-over-year by 28% in October. This statistic, often referred to as a leading market indicator, does not provide a very positive outlook for the near future. Most of the recent downturn in under contract may be attributed to the expiration of the federal tax credit, but other factors are also influencing the rapid drop in transactions including availability of credit and consumer expectations.

Residential settled sales plunged 32.4% in October when compared to the same time last year. The plummet was the largest year-over-year drop since January 2009, -35%. Each of the seven major cities in the area experienced sales declines ranging from a low of -21% in Norfolk to the high of -46% in Newport News. The median sales price for October 2010 was down 1.2% when compared to October 2009. The median price for homes sold seems to have bottomed for the region with its continued small differences as recorded each month. Some areas, including Virginia Beach, Chesapeake, and James City County, are starting to experience price appreciation with each area up 1% year-over-year.

The months’ supply of inventory held at ten months, but the absorption rate, the average number of homes sold over the past twelve months, continued to decline and is now at 1,480 homes per month.

The percentage of distressed listings, those that are bank owned or short sales, expanded to account for 22% of the active homes for sale and they comprised 31.7% of the settled sales total. October was, by far, the most prevalent month for distressed sales activity in our region since the housing bubble burst. Current market conditions and the overall economy do not show signs of a dramatic decrease in distressed listings. If these trends, both percent of active and sold listings, continue upward home prices within the region may decline as a result of the downward pressure these distressed homes have on local markets.

Tuesday, November 2, 2010

First Time Buyer Tips

RISMEDIA, May 25, 2010—Those who missed taking advantage of the first-time buyer tax credit but who are still planning the purchase of their first home, continue to have a wealth of opportunities in today’s marketplace. A few smart steps can save first-time buyers thousands of dollars. Here is a look at some of the ways how:

1. Don’t buy if you don’t plan to stayIf you can’t commit to remaining in one place for at least a few years, then owning is probably not for you, at least not yet. With the transaction costs of buying and selling a home, you may end up losing money if you sell any sooner – even in a rising market. When prices are falling, it’s an even worse proposition.

2. Start by shoring up your creditSince you probably will need to get a mortgage to buy a house, you must make sure your credit history is as clean as possible. A few months before you start house hunting, get copies of your credit report. Make sure the facts are correct, and fix any problems you discover.

3. Choose carefully between points and rateWhen picking a mortgage, you usually have the option of paying additional points- a portion of the interest that you pay at closing- in exchange for a lower interest rate. If you stay in the house for a long time- say three to five years or more- it’s usually a better deal to take the points. The lower interest rate will save you more in the long run.

4. Hire a home inspectorA home inspector can let you know if you’re about to buy a lemon of a house or warn you about potential problems. At best, you can move into the house confident that it’s in good shape; at worst, the inspector’s report can let you back out of the deal if the house has major, unexpected problems. Most typically, the home inspection can allow you to negotiate the home price to account for necessary repairs.

5. Get professional helpEven though the Internet gives buyers unprecedented access to home listings, most new buyers (and many more experienced ones) are better off using a professional agent. Look for an exclusive buyer agent, if possible, who will have your interests at heart and can help you with strategies during the bidding process.

6. Bonus Tip: Be patientBuying a home is one of the largest purchases most people will make in their lifetime. The key to avoiding buyer’s remorse is to be completely comfortable before signing on the dotted line.

Dan Steward is president, Pillar To Post.

{kind=link}

1. Don’t buy if you don’t plan to stayIf you can’t commit to remaining in one place for at least a few years, then owning is probably not for you, at least not yet. With the transaction costs of buying and selling a home, you may end up losing money if you sell any sooner – even in a rising market. When prices are falling, it’s an even worse proposition.

2. Start by shoring up your creditSince you probably will need to get a mortgage to buy a house, you must make sure your credit history is as clean as possible. A few months before you start house hunting, get copies of your credit report. Make sure the facts are correct, and fix any problems you discover.

3. Choose carefully between points and rateWhen picking a mortgage, you usually have the option of paying additional points- a portion of the interest that you pay at closing- in exchange for a lower interest rate. If you stay in the house for a long time- say three to five years or more- it’s usually a better deal to take the points. The lower interest rate will save you more in the long run.

4. Hire a home inspectorA home inspector can let you know if you’re about to buy a lemon of a house or warn you about potential problems. At best, you can move into the house confident that it’s in good shape; at worst, the inspector’s report can let you back out of the deal if the house has major, unexpected problems. Most typically, the home inspection can allow you to negotiate the home price to account for necessary repairs.

5. Get professional helpEven though the Internet gives buyers unprecedented access to home listings, most new buyers (and many more experienced ones) are better off using a professional agent. Look for an exclusive buyer agent, if possible, who will have your interests at heart and can help you with strategies during the bidding process.

6. Bonus Tip: Be patientBuying a home is one of the largest purchases most people will make in their lifetime. The key to avoiding buyer’s remorse is to be completely comfortable before signing on the dotted line.

Dan Steward is president, Pillar To Post.

Subscribe to:

Comments (Atom)