Finally! On the uptrend, pending sales increased in October since bottoming in June, according to the National Association of REALTORS.

A "pending" or "under contract" sale, is a real estate sale that is non-contingent (ex: home inspection contingency removed)and is moving forward to closing.

Read more about this at

http://www.realtor.org/press_room/news_releases/2010/12/strong_phs

Happy Holidays Everyone! Have a happy, healthy and prosperous new year!

Thursday, December 23, 2010

Tuesday, November 23, 2010

Holiday closings in South Hampton Roads

I'd like to wish everyone a wonderful Thanksgiving!

http://hamptonroads.com/2010/11/holiday-closings-south-hampton-roads?cid=srch

http://hamptonroads.com/2010/11/holiday-closings-south-hampton-roads?cid=srch

Sunday, November 21, 2010

Tax Credit Effects on the Real Estate Market

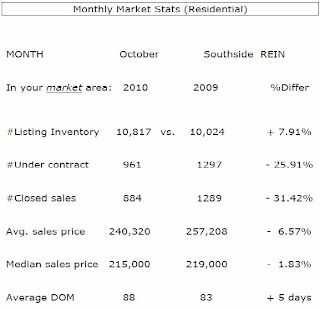

Last year's tax credit encouraged many buyers that were "sitting on the fence" to go ahead and purchase a new home. Here are the market stats for the month of October as it compares to this time last year.

REIN reports

Effects of ’09 Tax Credit Starting to Show

(Virginia Beach, Virginia – November 8, 2010)

The effects from the residential sales surge experienced in the third and fourth quarters of 2009 are now starting to be more prominent in 2010 sales totals comparisons. Traditionally, the third and fourth quarters are slower when compared to the second quarter of the year. But, in 2009 the third quarter had the highest sales total and the fourth quarter was almost equal to the second. This shift in buyers’ habits was due in large part to the federal tax credit. It caused many people who were potential buyers in the first and second quarters of 2010 to buy in the third and fourth quarters of 2009 prior to the original tax credit expiration of November 30. This date set a line in the sand for home buyers and the following extension allowed even more buyers to move their own purchase timelines to earlier dates thus “pulling forward” home sales activity. Many people across the country bought homes sooner than planned specifically for the tax credit and skewed many settled sales totals prior to the credit’s expiration.

The number of active homes for sale in the region last month remained high and increased by 8.95% when compared to October 2009. The recent levels of homes for sale have been the highest recorded for each month since February 2010. The region has maintained a level above 15,000 available listings for seven straight months, also the most on record. However, the median listing price of homes on the market in October 2010 declined by 9% when compared to October 2009. This drop is in line with the settling of home prices in Hampton Roads and is a potential sign of housing stability.

The number of under contract residential sales fell year-over-year by 28% in October. This statistic, often referred to as a leading market indicator, does not provide a very positive outlook for the near future. Most of the recent downturn in under contract may be attributed to the expiration of the federal tax credit, but other factors are also influencing the rapid drop in transactions including availability of credit and consumer expectations.

Residential settled sales plunged 32.4% in October when compared to the same time last year. The plummet was the largest year-over-year drop since January 2009, -35%. Each of the seven major cities in the area experienced sales declines ranging from a low of -21% in Norfolk to the high of -46% in Newport News. The median sales price for October 2010 was down 1.2% when compared to October 2009. The median price for homes sold seems to have bottomed for the region with its continued small differences as recorded each month. Some areas, including Virginia Beach, Chesapeake, and James City County, are starting to experience price appreciation with each area up 1% year-over-year.

The months’ supply of inventory held at ten months, but the absorption rate, the average number of homes sold over the past twelve months, continued to decline and is now at 1,480 homes per month.

The percentage of distressed listings, those that are bank owned or short sales, expanded to account for 22% of the active homes for sale and they comprised 31.7% of the settled sales total. October was, by far, the most prevalent month for distressed sales activity in our region since the housing bubble burst. Current market conditions and the overall economy do not show signs of a dramatic decrease in distressed listings. If these trends, both percent of active and sold listings, continue upward home prices within the region may decline as a result of the downward pressure these distressed homes have on local markets.

REIN reports

Effects of ’09 Tax Credit Starting to Show

(Virginia Beach, Virginia – November 8, 2010)

The effects from the residential sales surge experienced in the third and fourth quarters of 2009 are now starting to be more prominent in 2010 sales totals comparisons. Traditionally, the third and fourth quarters are slower when compared to the second quarter of the year. But, in 2009 the third quarter had the highest sales total and the fourth quarter was almost equal to the second. This shift in buyers’ habits was due in large part to the federal tax credit. It caused many people who were potential buyers in the first and second quarters of 2010 to buy in the third and fourth quarters of 2009 prior to the original tax credit expiration of November 30. This date set a line in the sand for home buyers and the following extension allowed even more buyers to move their own purchase timelines to earlier dates thus “pulling forward” home sales activity. Many people across the country bought homes sooner than planned specifically for the tax credit and skewed many settled sales totals prior to the credit’s expiration.

The number of active homes for sale in the region last month remained high and increased by 8.95% when compared to October 2009. The recent levels of homes for sale have been the highest recorded for each month since February 2010. The region has maintained a level above 15,000 available listings for seven straight months, also the most on record. However, the median listing price of homes on the market in October 2010 declined by 9% when compared to October 2009. This drop is in line with the settling of home prices in Hampton Roads and is a potential sign of housing stability.

The number of under contract residential sales fell year-over-year by 28% in October. This statistic, often referred to as a leading market indicator, does not provide a very positive outlook for the near future. Most of the recent downturn in under contract may be attributed to the expiration of the federal tax credit, but other factors are also influencing the rapid drop in transactions including availability of credit and consumer expectations.

Residential settled sales plunged 32.4% in October when compared to the same time last year. The plummet was the largest year-over-year drop since January 2009, -35%. Each of the seven major cities in the area experienced sales declines ranging from a low of -21% in Norfolk to the high of -46% in Newport News. The median sales price for October 2010 was down 1.2% when compared to October 2009. The median price for homes sold seems to have bottomed for the region with its continued small differences as recorded each month. Some areas, including Virginia Beach, Chesapeake, and James City County, are starting to experience price appreciation with each area up 1% year-over-year.

The months’ supply of inventory held at ten months, but the absorption rate, the average number of homes sold over the past twelve months, continued to decline and is now at 1,480 homes per month.

The percentage of distressed listings, those that are bank owned or short sales, expanded to account for 22% of the active homes for sale and they comprised 31.7% of the settled sales total. October was, by far, the most prevalent month for distressed sales activity in our region since the housing bubble burst. Current market conditions and the overall economy do not show signs of a dramatic decrease in distressed listings. If these trends, both percent of active and sold listings, continue upward home prices within the region may decline as a result of the downward pressure these distressed homes have on local markets.

Tuesday, November 2, 2010

Home Buyers and Sellers Dos an Don'ts

Be Market-Smart: Dos and Don'ts for Home Sellers and Buyers

By Dan Steward

It would be unrealistic to say that the real estate market is utterly rosy right now, but neither is it thorn-filled by any means. In fact, things are decidedly looking up: July got some good news, when the National Association of Realtors reported that pending home sales rose 5.2% from downwardly revised June levels, beating economists' expectations. This is good news for both buyers and sellers.

While challenges still exist-for instance, getting the best price when selling, or securing financing when buying-there are some once-in-a-lifetime opportunities out there, and plenty of happy results can be had for both buyers and sellers. The key for both groups is to remain flexible, adaptable and diligent. To that end, here are some dos and don'ts for today's buyers and sellers:

For Sellers:

DO'S

Be flexible. Often it's the little things that push a buyer into the "yes" zone. If the buyer goes on and on about how much they love your icemaker, throw it in. If the closing has to be pushed ahead more than you expected, try to be as flexible as possible and pack the moving van a little quicker.

Clean up. One person's prize doll collection is another person's cluttered nightmare. Similarly, a living room filled with Beanie Babies could elicit a reaction of fear, rather than "Aw, how cute!" from a buyer. Put away any personal collections that not only cause clutter, but also make it hard for a buyer to see the home as his or hers, rather than yours.

DON'TS

Don't be greedy. The market-not your emotions-dictates your home's price. If comparables in the area, and several trusted real estate agents tell you your home is worth $400,000, you're not fooling anyone by pricing it at $500,000-and you're only doing yourself a disservice. Pricing it at market, even a little below, could generate a bidding war, and ultimately get you more money.

Don't get personal. If you're selling your house for a certain amount, and someone offers something much lower, don't take this as a personal affront and refuse to counteroffer. Letting your emotions get in the way can potentially ruin the deal. What's the harm in making a counteroffer?

Don't procrastinate. In the current climate, you might be scared to try to sell your home, as you may have to face a lower selling price than you may have gotten before the recession. But remember, the house you buy might be even lower, commensurately. It's all relative. So if you're serious about selling, consider doing it now. Also, acting before the cold months come is a good idea, as the winter months are historically harder for home sales.

For Buyers:

DO'S

Get a home inspection. It's important to hire a trusted home inspector to check out the house's potential issues and problems. Don't skip a home inspection because you're afraid of what you might hear-many issues sound more serious than they actually are, and can be fixed easily. And if something deal-breakingly serious is turned up, as disappointing as that is, it can save years of heartache and financial outlay. Better to walk away from a clunker.

List your place before you look for another. If you're truly serious about looking for a home, list your place first. In the current economy, banks want to make sales as uncomplicated as possible-and contingency sales, which can be very complicated, are often rejected.

Talk before you act. Don't ever start a home search without a firm budget not only in mind, but literally written down. Mutually agree with yourself-or with your partner, if you're buying with someone else-long before you start seriously searching. Going out of that zone because of a place you just "gotta have," or are emotional about, could put you in dire financial straits later. You don't want to buy a house that isn't affordable for you, and then be worried about paying for dinner and a movie on Saturday night.

DON'TS

Don't be a design snob. If someone's enormous bathroom has wallpaper border containing frolicking kittens and pastel flowers, or a wall that's a nuclear shade of green, we understand this can send you into style shock. But stand fast and ignore bad d?cor. Instead, try to envision the space raw. Besides, you can always redecorate once the home is yours.

Don't make a silly offer. There's nothing wrong with making an offer below asking price-it's no secret that today, many homes are selling for under the asking price. But going 40% below the asking price may anger the seller. Some sellers, especially more emotional ones, won't even bother counter offering an outrageously low offer. Feel free to make a deal-just don't make an offer so low that you'll be kicked off the table.

By Dan Steward

It would be unrealistic to say that the real estate market is utterly rosy right now, but neither is it thorn-filled by any means. In fact, things are decidedly looking up: July got some good news, when the National Association of Realtors reported that pending home sales rose 5.2% from downwardly revised June levels, beating economists' expectations. This is good news for both buyers and sellers.

While challenges still exist-for instance, getting the best price when selling, or securing financing when buying-there are some once-in-a-lifetime opportunities out there, and plenty of happy results can be had for both buyers and sellers. The key for both groups is to remain flexible, adaptable and diligent. To that end, here are some dos and don'ts for today's buyers and sellers:

For Sellers:

DO'S

Be flexible. Often it's the little things that push a buyer into the "yes" zone. If the buyer goes on and on about how much they love your icemaker, throw it in. If the closing has to be pushed ahead more than you expected, try to be as flexible as possible and pack the moving van a little quicker.

Clean up. One person's prize doll collection is another person's cluttered nightmare. Similarly, a living room filled with Beanie Babies could elicit a reaction of fear, rather than "Aw, how cute!" from a buyer. Put away any personal collections that not only cause clutter, but also make it hard for a buyer to see the home as his or hers, rather than yours.

DON'TS

Don't be greedy. The market-not your emotions-dictates your home's price. If comparables in the area, and several trusted real estate agents tell you your home is worth $400,000, you're not fooling anyone by pricing it at $500,000-and you're only doing yourself a disservice. Pricing it at market, even a little below, could generate a bidding war, and ultimately get you more money.

Don't get personal. If you're selling your house for a certain amount, and someone offers something much lower, don't take this as a personal affront and refuse to counteroffer. Letting your emotions get in the way can potentially ruin the deal. What's the harm in making a counteroffer?

Don't procrastinate. In the current climate, you might be scared to try to sell your home, as you may have to face a lower selling price than you may have gotten before the recession. But remember, the house you buy might be even lower, commensurately. It's all relative. So if you're serious about selling, consider doing it now. Also, acting before the cold months come is a good idea, as the winter months are historically harder for home sales.

For Buyers:

DO'S

Get a home inspection. It's important to hire a trusted home inspector to check out the house's potential issues and problems. Don't skip a home inspection because you're afraid of what you might hear-many issues sound more serious than they actually are, and can be fixed easily. And if something deal-breakingly serious is turned up, as disappointing as that is, it can save years of heartache and financial outlay. Better to walk away from a clunker.

List your place before you look for another. If you're truly serious about looking for a home, list your place first. In the current economy, banks want to make sales as uncomplicated as possible-and contingency sales, which can be very complicated, are often rejected.

Talk before you act. Don't ever start a home search without a firm budget not only in mind, but literally written down. Mutually agree with yourself-or with your partner, if you're buying with someone else-long before you start seriously searching. Going out of that zone because of a place you just "gotta have," or are emotional about, could put you in dire financial straits later. You don't want to buy a house that isn't affordable for you, and then be worried about paying for dinner and a movie on Saturday night.

DON'TS

Don't be a design snob. If someone's enormous bathroom has wallpaper border containing frolicking kittens and pastel flowers, or a wall that's a nuclear shade of green, we understand this can send you into style shock. But stand fast and ignore bad d?cor. Instead, try to envision the space raw. Besides, you can always redecorate once the home is yours.

Don't make a silly offer. There's nothing wrong with making an offer below asking price-it's no secret that today, many homes are selling for under the asking price. But going 40% below the asking price may anger the seller. Some sellers, especially more emotional ones, won't even bother counter offering an outrageously low offer. Feel free to make a deal-just don't make an offer so low that you'll be kicked off the table.

First Time Buyer Tips

RISMEDIA, May 25, 2010—Those who missed taking advantage of the first-time buyer tax credit but who are still planning the purchase of their first home, continue to have a wealth of opportunities in today’s marketplace. A few smart steps can save first-time buyers thousands of dollars. Here is a look at some of the ways how:

1. Don’t buy if you don’t plan to stayIf you can’t commit to remaining in one place for at least a few years, then owning is probably not for you, at least not yet. With the transaction costs of buying and selling a home, you may end up losing money if you sell any sooner – even in a rising market. When prices are falling, it’s an even worse proposition.

2. Start by shoring up your creditSince you probably will need to get a mortgage to buy a house, you must make sure your credit history is as clean as possible. A few months before you start house hunting, get copies of your credit report. Make sure the facts are correct, and fix any problems you discover.

3. Choose carefully between points and rateWhen picking a mortgage, you usually have the option of paying additional points- a portion of the interest that you pay at closing- in exchange for a lower interest rate. If you stay in the house for a long time- say three to five years or more- it’s usually a better deal to take the points. The lower interest rate will save you more in the long run.

4. Hire a home inspectorA home inspector can let you know if you’re about to buy a lemon of a house or warn you about potential problems. At best, you can move into the house confident that it’s in good shape; at worst, the inspector’s report can let you back out of the deal if the house has major, unexpected problems. Most typically, the home inspection can allow you to negotiate the home price to account for necessary repairs.

5. Get professional helpEven though the Internet gives buyers unprecedented access to home listings, most new buyers (and many more experienced ones) are better off using a professional agent. Look for an exclusive buyer agent, if possible, who will have your interests at heart and can help you with strategies during the bidding process.

6. Bonus Tip: Be patientBuying a home is one of the largest purchases most people will make in their lifetime. The key to avoiding buyer’s remorse is to be completely comfortable before signing on the dotted line.

Dan Steward is president, Pillar To Post.

{kind=link}

1. Don’t buy if you don’t plan to stayIf you can’t commit to remaining in one place for at least a few years, then owning is probably not for you, at least not yet. With the transaction costs of buying and selling a home, you may end up losing money if you sell any sooner – even in a rising market. When prices are falling, it’s an even worse proposition.

2. Start by shoring up your creditSince you probably will need to get a mortgage to buy a house, you must make sure your credit history is as clean as possible. A few months before you start house hunting, get copies of your credit report. Make sure the facts are correct, and fix any problems you discover.

3. Choose carefully between points and rateWhen picking a mortgage, you usually have the option of paying additional points- a portion of the interest that you pay at closing- in exchange for a lower interest rate. If you stay in the house for a long time- say three to five years or more- it’s usually a better deal to take the points. The lower interest rate will save you more in the long run.

4. Hire a home inspectorA home inspector can let you know if you’re about to buy a lemon of a house or warn you about potential problems. At best, you can move into the house confident that it’s in good shape; at worst, the inspector’s report can let you back out of the deal if the house has major, unexpected problems. Most typically, the home inspection can allow you to negotiate the home price to account for necessary repairs.

5. Get professional helpEven though the Internet gives buyers unprecedented access to home listings, most new buyers (and many more experienced ones) are better off using a professional agent. Look for an exclusive buyer agent, if possible, who will have your interests at heart and can help you with strategies during the bidding process.

6. Bonus Tip: Be patientBuying a home is one of the largest purchases most people will make in their lifetime. The key to avoiding buyer’s remorse is to be completely comfortable before signing on the dotted line.

Dan Steward is president, Pillar To Post.

Risk Declines In Owning A Home

According to award winning Blanche Evans, real estate expert:

Home prices are up, foreclosures are down, and the demand for mortgage loans is up - all trends that collectively signal that owning a home is not as risky as it’s been in recent years.

A new report by Clear Capital, an asset valuation data services provider, has found that housing prices in Q2 2010 rose 7.9% over the first quarter, and that sales momentum continued through June, taking only the slightest breather.

Year over year, prices were up 8.1% for the quarter. Among the reasons is a drop in bank-owned properties, to 22.l7%, which is 19.8% below the peak set in Q1 2009. Prices are 13.6% on steady growth since reaching a trough, also in Q1 2009, according to Dr. Alex Villacorta, senior statistician for Clear Capital.

By August, mortgage interest rates are at an all-time low. Benchmark 30-year, fixed-rates fell to the lowest levels since 1971, at 4.44%, spurring demand for refinancing as well as purchase loans. The Mortgage Bankers Association says that demand steadily increased through mid-August on record low rates. A year ago, interest rates were 5.17%.

Adding to the good news was the Commerce Department, which announced 1.7% more construction on home in July 2010 than the previous month.

The National Association of REALTORS® (NAR) also noted an increase of 1.5% in pending home sales, suggesting that demand for housing is growing again.

Following the expiration of the homebuyer tax credit which hurried sales forward for hurry-up buyers, both new home and existing home sales declined, prompting speculation that home prices would take a double dip from the last decline in 2009. In Q2 2010, the NAR found that 100 out of 155 metropolitan statistical areas reported higher median existing single-family home prices, including 14 with a double-digit increase.

Among the reasons for the improvement was fewer distressed homes were sold, only 32% of Q2 sales from 36% the year before.

Explains Lawrence Yun, chief economist for the NAR, “The recorded home prices in many markets were significantly depressed last year because of a large percentage of distressed homes sold at discount. Now as more normal, non-distressed home sales are occurring, the median price in many areas is showing higher values.”

In August 2010, the PMI Group, Inc., reflected the collective sigh of relief with a lower U.S. Market Risk Index. Using Q1 2010 data, the mortgage risk insurer noted that its index dropped to 51.9 from 53.8 for a third consecutive quarterly decrease.

Of the nation’s metropolitan statistical areas, 290 or 75.5% are pose less risk for housing than the previous quarter. That said, more than half, or 51.6% are still in PMI’s high-risk category, with higher unemployment rates, higher foreclosure rates, lower affordability, a larger excess housing supply, or more volatile housing prices than other MSAs with minimal to moderate risks.

But as other economists have found, there is a slow but steady improvement in economic indicators including home price appreciation, mortgage market affordability, employment, housing affordability returning to median norms, and lower foreclosure activity.

"Household formation is the most important demographic driver of housing demand and faster growth, as has occurred over the period since the middle of 2009,” explains David Berson, PMI chief economist, “corresponding to a pickup in the economy, should lead to greater market stability. "Ultimately greater stability of house prices will lead to declines in the Risk Index."

Home prices are up, foreclosures are down, and the demand for mortgage loans is up - all trends that collectively signal that owning a home is not as risky as it’s been in recent years.

A new report by Clear Capital, an asset valuation data services provider, has found that housing prices in Q2 2010 rose 7.9% over the first quarter, and that sales momentum continued through June, taking only the slightest breather.

Year over year, prices were up 8.1% for the quarter. Among the reasons is a drop in bank-owned properties, to 22.l7%, which is 19.8% below the peak set in Q1 2009. Prices are 13.6% on steady growth since reaching a trough, also in Q1 2009, according to Dr. Alex Villacorta, senior statistician for Clear Capital.

By August, mortgage interest rates are at an all-time low. Benchmark 30-year, fixed-rates fell to the lowest levels since 1971, at 4.44%, spurring demand for refinancing as well as purchase loans. The Mortgage Bankers Association says that demand steadily increased through mid-August on record low rates. A year ago, interest rates were 5.17%.

Adding to the good news was the Commerce Department, which announced 1.7% more construction on home in July 2010 than the previous month.

The National Association of REALTORS® (NAR) also noted an increase of 1.5% in pending home sales, suggesting that demand for housing is growing again.

Following the expiration of the homebuyer tax credit which hurried sales forward for hurry-up buyers, both new home and existing home sales declined, prompting speculation that home prices would take a double dip from the last decline in 2009. In Q2 2010, the NAR found that 100 out of 155 metropolitan statistical areas reported higher median existing single-family home prices, including 14 with a double-digit increase.

Among the reasons for the improvement was fewer distressed homes were sold, only 32% of Q2 sales from 36% the year before.

Explains Lawrence Yun, chief economist for the NAR, “The recorded home prices in many markets were significantly depressed last year because of a large percentage of distressed homes sold at discount. Now as more normal, non-distressed home sales are occurring, the median price in many areas is showing higher values.”

In August 2010, the PMI Group, Inc., reflected the collective sigh of relief with a lower U.S. Market Risk Index. Using Q1 2010 data, the mortgage risk insurer noted that its index dropped to 51.9 from 53.8 for a third consecutive quarterly decrease.

Of the nation’s metropolitan statistical areas, 290 or 75.5% are pose less risk for housing than the previous quarter. That said, more than half, or 51.6% are still in PMI’s high-risk category, with higher unemployment rates, higher foreclosure rates, lower affordability, a larger excess housing supply, or more volatile housing prices than other MSAs with minimal to moderate risks.

But as other economists have found, there is a slow but steady improvement in economic indicators including home price appreciation, mortgage market affordability, employment, housing affordability returning to median norms, and lower foreclosure activity.

"Household formation is the most important demographic driver of housing demand and faster growth, as has occurred over the period since the middle of 2009,” explains David Berson, PMI chief economist, “corresponding to a pickup in the economy, should lead to greater market stability. "Ultimately greater stability of house prices will lead to declines in the Risk Index."

Wednesday, October 27, 2010

International Buyers Investing in U.S. Housing Market

International Buyers of Real Estate on the Rise

October 20, 2010

Thanks to the low prices that can be found on real estate throughout the United States, many foreign investors are turning their attention away from the U.S. stock market and putting their attention on the housing market instead. In fact, foreign investment in U.S. real estate has virtually skyrocketed recently, with most planning to rent out the properties and then to sell them once the economy turns around.

Given the prices that real estate investors have before them, it is easy to see why the interest has grown. At the Viceroy condos in downtown Miami, for example, units once sold for as high as $670 per square foot. Today, they can be purchased at an average price of $319 per square foot.

“I have never seen such a high concentration of foreign nationals acquiring real estate,” said Peter Zalewski in a recent Yahoo finance article. “Eight percent of the sales in downtown Miami are foreign-based. This is unprecendented.”

Miami isn’t the only market to see an increase in foreign investors, however, as other hot spots have included New York, Washington, Las Vegas, San Francisco, Los Angeles, Seattle and Phoenix. In fact, Phoenix saw more buyers from Canada than from California for the first time recently.

“It’s a positive in a sea of negatives,” said Jonathan Miller, who is the chief executive of Miller Samuel, which is a New York-based real estate consulting firm.

Even better for those with money to invest, the payoff can start immediately. Some, for example, focus solely on purchasing those condos that already have renters. In this way, he is able to immediately walk away each month with a profit after paying association fees and taxes. In short, the weak currency, high unemployment and expansive inventory have made the United States an attractive buyer’s market.

“Never before have all these things come together like this,” said Patrick O’Neill, who is the chief executive officer of the O’Neill Group in Hong Kong. “Unless you want to go to Baghdad, the United States is the best you can get.”

The National Association of Realtors is also reporting an increase in international sales, as 28% of brokers have reported working with at least one international client. This figure is up by 5% when compared to last year. Similarly, 8% of brokers report completing at least one sale with an international client, which is up from 12% in 2009.

“I was going [to] invest in the stock market, but I decided to invest in real estate instead,” said Diego Garcia, who is a native of Mexico City and is on assignment with Pfizer Inc. in New York City.

Of course, there are still risks involved with making this type of purchase, as the housing market is still far from reaching a full recovery. Furthermore, prices are still continuing to fall in many markets, which means a foreign investor could get stuck in a bad situation if needing to make a quick sale. Similarly, if a renter leaves, the investor will be stuck without any cash coming in. Nonetheless, demand from foreign investors continues to grow. In fact, overseas buyers now represent 7% of the total buyer’s market. In response, many U.S. brokerages are now hiring agents who are able to speak foreign languages.

“The international buyer pool is better than we have ever seen it before,” said Phillip White, who is the president of New York-based Sotheby’s International.

October 20, 2010

Thanks to the low prices that can be found on real estate throughout the United States, many foreign investors are turning their attention away from the U.S. stock market and putting their attention on the housing market instead. In fact, foreign investment in U.S. real estate has virtually skyrocketed recently, with most planning to rent out the properties and then to sell them once the economy turns around.

Given the prices that real estate investors have before them, it is easy to see why the interest has grown. At the Viceroy condos in downtown Miami, for example, units once sold for as high as $670 per square foot. Today, they can be purchased at an average price of $319 per square foot.

“I have never seen such a high concentration of foreign nationals acquiring real estate,” said Peter Zalewski in a recent Yahoo finance article. “Eight percent of the sales in downtown Miami are foreign-based. This is unprecendented.”

Miami isn’t the only market to see an increase in foreign investors, however, as other hot spots have included New York, Washington, Las Vegas, San Francisco, Los Angeles, Seattle and Phoenix. In fact, Phoenix saw more buyers from Canada than from California for the first time recently.

“It’s a positive in a sea of negatives,” said Jonathan Miller, who is the chief executive of Miller Samuel, which is a New York-based real estate consulting firm.

Even better for those with money to invest, the payoff can start immediately. Some, for example, focus solely on purchasing those condos that already have renters. In this way, he is able to immediately walk away each month with a profit after paying association fees and taxes. In short, the weak currency, high unemployment and expansive inventory have made the United States an attractive buyer’s market.

“Never before have all these things come together like this,” said Patrick O’Neill, who is the chief executive officer of the O’Neill Group in Hong Kong. “Unless you want to go to Baghdad, the United States is the best you can get.”

The National Association of Realtors is also reporting an increase in international sales, as 28% of brokers have reported working with at least one international client. This figure is up by 5% when compared to last year. Similarly, 8% of brokers report completing at least one sale with an international client, which is up from 12% in 2009.

“I was going [to] invest in the stock market, but I decided to invest in real estate instead,” said Diego Garcia, who is a native of Mexico City and is on assignment with Pfizer Inc. in New York City.

Of course, there are still risks involved with making this type of purchase, as the housing market is still far from reaching a full recovery. Furthermore, prices are still continuing to fall in many markets, which means a foreign investor could get stuck in a bad situation if needing to make a quick sale. Similarly, if a renter leaves, the investor will be stuck without any cash coming in. Nonetheless, demand from foreign investors continues to grow. In fact, overseas buyers now represent 7% of the total buyer’s market. In response, many U.S. brokerages are now hiring agents who are able to speak foreign languages.

“The international buyer pool is better than we have ever seen it before,” said Phillip White, who is the president of New York-based Sotheby’s International.

Monday, October 25, 2010

Don't be Scared to Buy a Home

Buying a Home Shouldn’t Be Scary

by Nancy Chandler Associates, REALTORS on Tuesday, October 12, 2010 at 3:47pm

As Halloween approaches, you might wonder if this is a good time to consider buying a home in Virginia Beach. Will you be spooked by housing costs and condo fees and real estate jargon that turns you white as a ghost because you don’t understand it. Trust us when we say that bidding on a home for sale needn’t be scary – with the right Realtor to show you all the best “haunts” suited to your family and lifestyle, you can still find a terrific deal for your needs and budget.

One plus to house hunting in October is this gorgeous Fall weather we’re currently enjoying. Here you’ll truly see neighborhoods at their most active. You’ll get a feel for various dynamics – kids at play, weekend warriors tackling their landscapes – and traffic low in the off-season. Especially if you have children, you’ll want to pay attention to school districts and opportunities for extracurricular fun, like proximity to the beach and aquarium and other favorite family spots. Some neighborhood associations may sponsor seasonal gatherings or block-wide yard sales as a sign of solid community. As real estate professionals who know the Norfolk/Virginia Beach areas, we are more than aptly qualified to match the community to your needs.

This year, as you prepare for Halloween and get your kids’ costumes ready, why not do some trick or treating of your own and check out our available listings for homes in Norfolk and Virginia Beach. What we have to offer will definitely keep you cozy through all the holidays.

Sunday, October 17, 2010

Hampton Roads Real Estate..Have we finally hit bottom??

Tuesday, October 12, 2010 — Though economists have marked many milestones as the alleged bottom of the housing market, according to Beacon researchers, current home affordability is pointing to the worst being behind us.

Beacon Economics analyzed home affordability and came away feeling optimistic.Beacon Economics founding principal Christopher Thornberg, whose firm advises a variety of business clients, says the high level of affordability is likely to drive demand and reduce the stock of excess inventory, ultimately resulting in the need for new housing, a rise in prices, and a pickup in new construction."While prices may fluctuate modestly over the next several months, we believe the worst of the housing crisis is behind us," says Beacon Economics Research Manager Jordan G. Levine. "We expect prices to stabilize around current levels and likely be higher in the next 12 months." It's a great time to buy..interest rates are at an all time low and housing prices have bottomed out!! I can help you with all of your real estate needs!

Beacon Economics analyzed home affordability and came away feeling optimistic.Beacon Economics founding principal Christopher Thornberg, whose firm advises a variety of business clients, says the high level of affordability is likely to drive demand and reduce the stock of excess inventory, ultimately resulting in the need for new housing, a rise in prices, and a pickup in new construction."While prices may fluctuate modestly over the next several months, we believe the worst of the housing crisis is behind us," says Beacon Economics Research Manager Jordan G. Levine. "We expect prices to stabilize around current levels and likely be higher in the next 12 months." It's a great time to buy..interest rates are at an all time low and housing prices have bottomed out!! I can help you with all of your real estate needs!

Subscribe to:

Posts (Atom)